Contribution Margin: Definition, Overview, and How To Calculate

October 4, 2021

In this chapter, we begin examining the relationship among sales volume, fixed costs, variable costs, and profit in decision-making. We will discuss how to use the concepts of fixed and variable costs and their relationship to profit to determine the sales needed to break even or to reach a desired profit. You will also learn how to plan for changes in selling price or costs, whether a single product, multiple products, or services are involved. Therefore, the unit contribution margin (selling price per unit minus variable costs per unit) is $3.05. The company’s contribution margin of $3.05 will cover fixed costs of $2.33, contributing $0.72 to profits.

Unit Contribution Margin

Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion for teaching. After almost a decade of experience in public accounting, he created MyAccountingCourse.com to help people learn accounting & finance, pass the CPA exam, and start their career.

Ask Any Financial Question

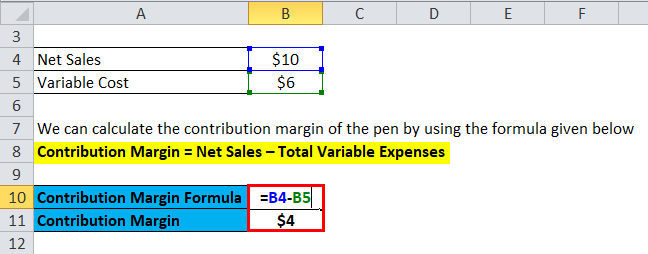

In the United States, similar labor-saving processes have been developed, such as the ability to order groceries or fast food online and have it ready when the customer arrives. Do these labor-saving processes change the cost structure for the company? The first step to calculate the contribution margin is to determine the net sales of your business. Net sales refer to the total revenue your business generates as a result of selling its goods or services. Dobson Books Company sells textbook sets to primary and high schools.

Everything You Need To Master Financial Modeling

As a result, a high contribution margin would help you in covering the fixed costs of your business. To calculate contribution margin (CM) by product, calculate it for each product on a per-unit basis. After you’ve completed the unit contribution margin calculation, you can also determine the contribution margin by product in total dollars.

Weighted average contribution margin per unit equals the sum of contribution margins of all products divided by total units. Weighted average contribution margin ratio equals the sum of contribution margins of all products divided by total sales. As another step, you can compute the cash breakeven point using cash-based variable costs and fixed costs.

So, it is an important financial ratio to examine the effectiveness of your business operations. Sales revenue refers to the total income your business generates as a result of selling goods or services. Furthermore, sales revenue can be categorized into gross and net sales revenue. Furthermore, it also gives you an understanding of the amount of profit you can generate after covering your fixed cost.

Compare the lines for determining accrual basis breakeven and cash breakeven on a graph showing different volume levels. Gross margin is calculated before you deduct operating expenses shown in the income statement to reach operating income. Each profit measure can be expressed as total dollars or as a ratio that is a percentage of the total amount of revenue. The variable costs to produce the baseball include direct raw materials, direct labor, and other direct production costs that vary with volume. However, an ideal contribution margin analysis will cover both fixed and variable cost and help the business calculate the breakeven. A high margin means the profit portion remaining in the business is more.

- Management uses this metric to understand what price they are able to charge for a product without losing money as production increases and scale continues.

- The contribution margin is the leftover revenue after variable costs have been covered and it is used to contribute to fixed costs.

- If total fixed cost is $466,000, the selling price per unit is $8.00, and the variable cost per unit is $4.95, then the contribution margin per unit is $3.05.

- Shaun Conrad is a Certified Public Accountant and CPA exam expert with a passion for teaching.

- This team of experts helps Finance Strategists maintain the highest level of accuracy and professionalism possible.

The contribution margin represents how much revenue remains after all variable costs have been paid. It is the amount of income available for contributing to fixed costs and profit and is the foundation of a company’s break-even analysis. Total contribution margin (TCM) is calculated by subtracting total variable costs from total sales.

This, in turn, can help people make better decisions regarding product & service pricing, product lines, and sales commissions or bonuses. The concept of contribution margin is applicable at various levels of manufacturing, business segments, and products. Where C is the contribution margin, R is the total revenue, and V represents variable costs. While there are plenty of profitability metrics—ranging from the gross margin down to the net profit margin—the contribution margin metric stands out for the analysis of a specific product or service.

Additionally, it assists in setting pricing strategies to ensure that products are priced appropriately to cover both variable and fixed costs while maximizing overall profitability. Overall, the unit contribution margin provides valuable insights into the financial performance of individual products or units and helps guide strategic decision-making within organizations. As mentioned above, contribution margin refers to the difference between sales revenue and variable costs of producing goods or services.

The contribution margin represents the revenue that a company gains by selling each additional unit of a product or good. This is one of several metrics that companies and investors use to make data-driven decisions about their business. As with other figures, it is important to consider contribution margins in relation to other metrics rather than in isolation. Profit factoring software made powerfully simple try it today margin is calculated using all expenses that directly go into producing the product. The formula to calculate the contribution margin is equal to revenue minus variable costs. Alternatively, companies that rely on shipping and delivery companies that use driverless technology may be faced with an increase in transportation or shipping costs (variable costs).